Gerald Kyalo. (geraldbway).

Gerald Kyalo. (geraldbway).

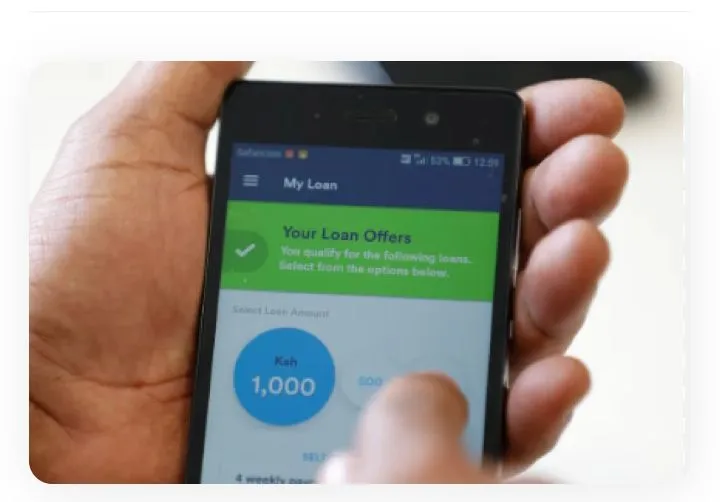

Mobile money loans are increasingly dominating Kenya’s credit market, reflecting the rapid rise in mobile money usage across the country and the wider Sub-Saharan Africa region. While this digital revolution has broadened access to finance for millions, it has also brought a surge in fraudulent activity, posing challenges to both providers and consumers.

According to the 2025 State of Industry Report by the global technology body GSMA, Sub-Saharan Africa continues to lead the global expansion of mobile money accounts. Of the 2.3 billion registered mobile money accounts worldwide, nearly two-thirds of the sector’s growth came from Africa, highlighting the region’s central role in driving financial inclusion.

Within the continent, Kenya, Tanzania, and Uganda boast the highest rates of mobile money account ownership in the world. In Kenya specifically, 20% of adults rely exclusively on mobile money for their financial transactions, underscoring a shift away from traditional banking systems. The GSMA report notes that as mobile money account ownership rises, a preference for borrowing through mobile platforms has emerged, with many consumers shunning conventional banks, microfinance institutions, and savings and credit cooperatives (SACCOs).

The survey found that mobile money borrowing now accounts for approximately 60% of all formal borrowing in Sub-Saharan Africa. In Kenya, 32% of adults accessed loans via mobile money providers (MMPs), while 25% rely solely on mobile loans, avoiding traditional financial institutions altogether.

“A larger share got a loan through a mobile money account in 2024. At the same time, bank-only borrowing decreased among those who borrowed exclusively this way,” the GSMA report observes. These loans are typically low-value and short-term, allowing rapid disbursement and repayment, which in turn has driven profitability for MMPs. Agents, who facilitate these transactions, play a crucial role in digitizing money and supporting financial inclusion across the country.

Despite the sector’s growth, fraud remains a significant threat. Globally, nearly $500 billion is lost annually to digital financial fraud, making it the most common complaint among consumers of digital financial services.

Mobile money users in Kenya and across Africa face multiple forms of fraud. Identity fraud is the most prevalent, but impersonation, insider fraud by MMP staff, agent fraud, and cyber fraud also occur. Other losses arise from social engineering and SIM swap schemes, where fraudsters manipulate users into giving up access to their accounts.

To counter these threats, MMPs have increasingly adopted Artificial Intelligence (AI) and Machine Learning (ML) solutions. These technologies enable providers to detect anomalies such as unusual transaction patterns in real-time. By training algorithms on historical fraud events, mobile money platforms can predict potentially fraudulent activities and prevent financial losses before they escalate.

In addition to technology-driven solutions, MMPs are also investing in consumer awareness campaigns to educate users on safe digital practices. However, the sector still grapples with challenges such as high taxation on mobile transactions, inconsistent licensing, high remittance costs, and gaps in infrastructure and policy.

Kenya’s government has played a pivotal role in promoting mobile lending and financial inclusion. In 2022, the Kenya Kwanza administration launched the Hustler Fund, a Financial Inclusion Fund disbursed through mobile money platforms. As of November 2025, over Ksh. 80 million had been distributed in personal loans and small business credits to previously underserved populations.

President William Ruto highlighted the program’s impact, stating, “We took a firm position and negotiated with credit reference bureaus and we redeemed 7 million Kenyans who were blacklisted, giving them a second chance. Today, we have 2 million Kenyans who borrow religiously from the Hustler Fund.”

In August 2025, the government introduced the National Youth Opportunities Towards Advancement (NYOTA) Project, a collaboration with the World Bank that provides Ksh. 50,000 in startup capital to youth and vulnerable groups historically excluded from formal credit systems. Both Hustler Fund and NYOTA loans can be accessed through mobile platforms using USSD codes, further cementing mobile money as a cornerstone of Kenya’s financial ecosystem.

Despite these initiatives, loan defaults have undermined progress. As of March 5, 2026, borrowers had defaulted on Ksh. 12 billion taken from the Hustler Fund. In response, the government has disqualified defaulters from accessing NYOTA funds and implemented stricter recovery measures, tracing defaulters through personal identifiers such as national IDs and SIM cards.

Reflecting these challenges, the 2025/26 budget for the Hustler Fund was reduced drastically to Ksh. 300 million from an initial allocation of Ksh. 5 billion, highlighting the need for sustainable loan management while continuing to expand access to credit.

Mobile money loans are reshaping financial access in Kenya, empowering millions who were previously excluded from formal banking. However, as the market grows, it must also contend with rising fraud, loan defaults, and regulatory challenges. Providers and the government are responding with technology-driven solutions, consumer education, and stricter recovery mechanisms, signaling a commitment to preserving the sector’s benefits while addressing its risks.

The Kenyan experience reflects a broader trend across Sub-Saharan Africa, where mobile money is not just a convenience but a critical driver of economic participation, particularly for low-income and underserved populations. The balance between inclusion and protection will be pivotal as the sector continues to evolve.

According to the 2025 State of Industry Report by the global technology body GSMA, Sub-Saharan Africa continues to lead the global expansion of mobile money accounts. Of the 2.3 billion registered mobile money accounts worldwide, nearly two-thirds of the sector’s growth came from Africa, highlighting the region’s central role in driving financial inclusion.

Within the continent, Kenya, Tanzania, and Uganda boast the highest rates of mobile money account ownership in the world. In Kenya specifically, 20% of adults rely exclusively on mobile money for their financial transactions, underscoring a shift away from traditional banking systems. The GSMA report notes that as mobile money account ownership rises, a preference for borrowing through mobile platforms has emerged, with many consumers shunning conventional banks, microfinance institutions, and savings and credit cooperatives (SACCOs).

The survey found that mobile money borrowing now accounts for approximately 60% of all formal borrowing in Sub-Saharan Africa. In Kenya, 32% of adults accessed loans via mobile money providers (MMPs), while 25% rely solely on mobile loans, avoiding traditional financial institutions altogether.

“A larger share got a loan through a mobile money account in 2024. At the same time, bank-only borrowing decreased among those who borrowed exclusively this way,” the GSMA report observes. These loans are typically low-value and short-term, allowing rapid disbursement and repayment, which in turn has driven profitability for MMPs. Agents, who facilitate these transactions, play a crucial role in digitizing money and supporting financial inclusion across the country.

Despite the sector’s growth, fraud remains a significant threat. Globally, nearly $500 billion is lost annually to digital financial fraud, making it the most common complaint among consumers of digital financial services.

Mobile money users in Kenya and across Africa face multiple forms of fraud. Identity fraud is the most prevalent, but impersonation, insider fraud by MMP staff, agent fraud, and cyber fraud also occur. Other losses arise from social engineering and SIM swap schemes, where fraudsters manipulate users into giving up access to their accounts.

To counter these threats, MMPs have increasingly adopted Artificial Intelligence (AI) and Machine Learning (ML) solutions. These technologies enable providers to detect anomalies such as unusual transaction patterns in real-time. By training algorithms on historical fraud events, mobile money platforms can predict potentially fraudulent activities and prevent financial losses before they escalate.

In addition to technology-driven solutions, MMPs are also investing in consumer awareness campaigns to educate users on safe digital practices. However, the sector still grapples with challenges such as high taxation on mobile transactions, inconsistent licensing, high remittance costs, and gaps in infrastructure and policy.

Kenya’s government has played a pivotal role in promoting mobile lending and financial inclusion. In 2022, the Kenya Kwanza administration launched the Hustler Fund, a Financial Inclusion Fund disbursed through mobile money platforms. As of November 2025, over Ksh. 80 million had been distributed in personal loans and small business credits to previously underserved populations.

President William Ruto highlighted the program’s impact, stating, “We took a firm position and negotiated with credit reference bureaus and we redeemed 7 million Kenyans who were blacklisted, giving them a second chance. Today, we have 2 million Kenyans who borrow religiously from the Hustler Fund.”

In August 2025, the government introduced the National Youth Opportunities Towards Advancement (NYOTA) Project, a collaboration with the World Bank that provides Ksh. 50,000 in startup capital to youth and vulnerable groups historically excluded from formal credit systems. Both Hustler Fund and NYOTA loans can be accessed through mobile platforms using USSD codes, further cementing mobile money as a cornerstone of Kenya’s financial ecosystem.

Despite these initiatives, loan defaults have undermined progress. As of March 5, 2026, borrowers had defaulted on Ksh. 12 billion taken from the Hustler Fund. In response, the government has disqualified defaulters from accessing NYOTA funds and implemented stricter recovery measures, tracing defaulters through personal identifiers such as national IDs and SIM cards.

Reflecting these challenges, the 2025/26 budget for the Hustler Fund was reduced drastically to Ksh. 300 million from an initial allocation of Ksh. 5 billion, highlighting the need for sustainable loan management while continuing to expand access to credit.

Mobile money loans are reshaping financial access in Kenya, empowering millions who were previously excluded from formal banking. However, as the market grows, it must also contend with rising fraud, loan defaults, and regulatory challenges. Providers and the government are responding with technology-driven solutions, consumer education, and stricter recovery mechanisms, signaling a commitment to preserving the sector’s benefits while addressing its risks.

The Kenyan experience reflects a broader trend across Sub-Saharan Africa, where mobile money is not just a convenience but a critical driver of economic participation, particularly for low-income and underserved populations. The balance between inclusion and protection will be pivotal as the sector continues to evolve.